Blog + News

Why the Alberta Budget Suggests that Alberta Resident Corporations May Want to Pay Out Retained Earnings Before January 1, 2021*

(*Updated on October 30, 2019 to reflect Bill 20)

Canada’s tax regime on corporate and dividend income is based on the integration theory. In practice, integration is often not perfect due to varying provincial corporate tax rates. This blog explains how the previous Alberta Government broke integration in 2015, and how the current Government’s corporate rate reductions and 2019 Alberta Budget released on October 24, 2019 bring Alberta corporate/shareholder taxation back to integration, but in doing so, creates a tax arbitrage trap for the unwary.

Simply put, tax integration stands for the proposition that the legal form through which income is earned (for example, in corporate form or personally) should not matter: the overall taxation load should be roughly the same. For instance, if a corporation earns income, then the extraction of any after-tax surplus to the personal shareholder and the underlying corporate tax should be roughly equal to what the overall tax would have been on personal income. In Alberta, the total corporate and shareholder tax load on corporate income should be, in theory, about 48% – the same as the top personal tax rate on income.

The basic mechanics of integration are as follows:

- Corporate income is first subject to corporate tax, which is akin to a down payment of tax. The rate of corporate tax may be either the lower small business rate or higher general rate, the former needing to meet specific criteria. For the sake of illustration, let’s assume $100 of corporate income is subject to the general corporate tax rate of 27%, so there is a corporate tax ‘down payment’ of $27;

- When the corporation distributes the $73 of after-tax corporate income to its shareholder(s) as a dividend, the shareholder is required to “gross-up” the dividend income inclusion on the personal tax return to reflect the original corporate income before the corporate tax. To accomplish this, a gross-up rate of approximately 38% would be needed to bring income back to $100 ($73 x 138% equals roughly $100); and

- The shareholder then computes personal tax based on the $100 grossed-up dividend. To give credit for the down payment of tax already made by the corporation (i.e. the $27 of corporate tax), the shareholder obtains a dividend tax credit that should equal the $27.

To account for the two different levels of corporate tax, the Income Tax Act uses the general rate income pool (“GRIP”) and “eligible dividend” system. Generally speaking, corporate income that is subject to the low small business rate can only be paid out to shareholders as non-eligible dividends. Non-eligible dividends are subject to a specific set of gross-up factor and dividend tax credit to reflect the lower corporate tax burden. Corporate income subject to the higher general corporate tax adds to the GRIP. It can be paid out as eligible dividends, which have a different set of gross-up factor and dividend tax credit.

In theory, when the corporate tax rate changes, the government should automatically adjust the gross-up factor and dividend tax credit. However, with Canada’s provincial tax system, this cannot be achieved perfectly. The federal Income Tax Act sets the gross-up factor and includes no customization for the different provincial corporate tax rates across Canada. On the other hand, because provinces set their dividend tax credit, there is no reason why a province cannot match the dividend tax credit to the corporate tax rate.

In 2015, this integrated system broke down in Alberta.

2015 to 2018

On June 30, 2015, the Alberta Government increased the general corporate tax rate from 10% to 12% (or 25% to 27%, when combined with the federal general corporate tax rate). Curiously, the Government at that time did not increase the dividend tax credit for eligible dividends to account for this – recall from the above discussion that corporate income subject to general corporate tax rate creates GRIP, which allows for payment of eligible dividends.

In contrast, Alberta has adjusted its dividend tax credit for non-eligible dividends each year since 2015 to keep overall taxation more or less perfectly integrated with corporate income subject to the small business tax rate. This includes the time when the Alberta small business corporate tax rate dropped 3% to 2% on January 1, 2017.

Therefore, by not increasing the eligible dividend tax credit for 2015 to 2018 simultaneously with the increase in the general corporate tax rate, the previous Alberta Government imposed a hidden tax increase for shareholders of public corporations and large private corporations. Below is a table of a fully integrated tax rate of such corporate income, including both corporate tax and personal tax from full distribution of after-tax corporate profits, from 2014 to 2018:

|

2014 |

2015 |

2016 |

2017 |

2018 |

|

|

Integrated tax rate on corporate income subject to the general corporate rate |

39.47% |

41.55% |

50.15% |

50.15% |

50.15% |

|

Compare to the top personal tax rate |

39% |

40.25% |

48.00% |

48.00% |

48.00% |

|

Additional tax cost of earning income corporately |

0.47% |

1.30% |

2.15% |

2.15% |

2.15% |

Notice that the integrated rates crept up significantly above the top Alberta personal tax rate of 48%, signifying the end of integration between the overall corporate/shareholder tax burden and personal tax rates. It was no longer tax neutral between earning income personally and earning corporate income that is subject to the general corporate tax rate, as the latter carries a tax penalty of 2.15%.

One reason for this policy decision may be that the traditional primary contributor to Alberta corporate tax, oil and gas producers, likely had little earnings and paid little to no corporate income tax during the period from 2015 to 2018 due to massive losses in this sector. The Government may have rationalized that an adjustment to the eligible dividend tax credit would just allow mostly pre-2015 corporate retained earnings (i.e. pre-tax increase) to be paid out at more favourable personal tax rates. Nevertheless, such non-integration goes against the fundamental principles of the Canadian tax system.

While the above is a fascinating history lesson for tax geeks like us at Moodys, the changes discussed below are more relevant. They will drive future investment decisions by business owners.

2019 to 2021

Soon after the current Alberta government was elected, it put forward in Bill 3 (since passed into law) a series of cuts to the Alberta corporate tax rate from 12% rate to 8% as follows:

- On July 1, 2019, a reduction of 1% to 11%;

- On January 1, 2020, a further reduction of 1% to 10%;

- On January 1, 2021, a further reduction of 1% to 9%; and

- On January 1, 2022, a final reduction of 1% to 8%.

The government announced no changes to the 2% small business corporate tax rate. As a quick aside, our firm is aware of some people calling the above reductions a $4.5B tax giveaway to the rich, and we respectfully disagree with such views. As explained above – the imposition of corporate tax is simply a down-payment on the overall tax that ultimately will be paid on an integrated basis.

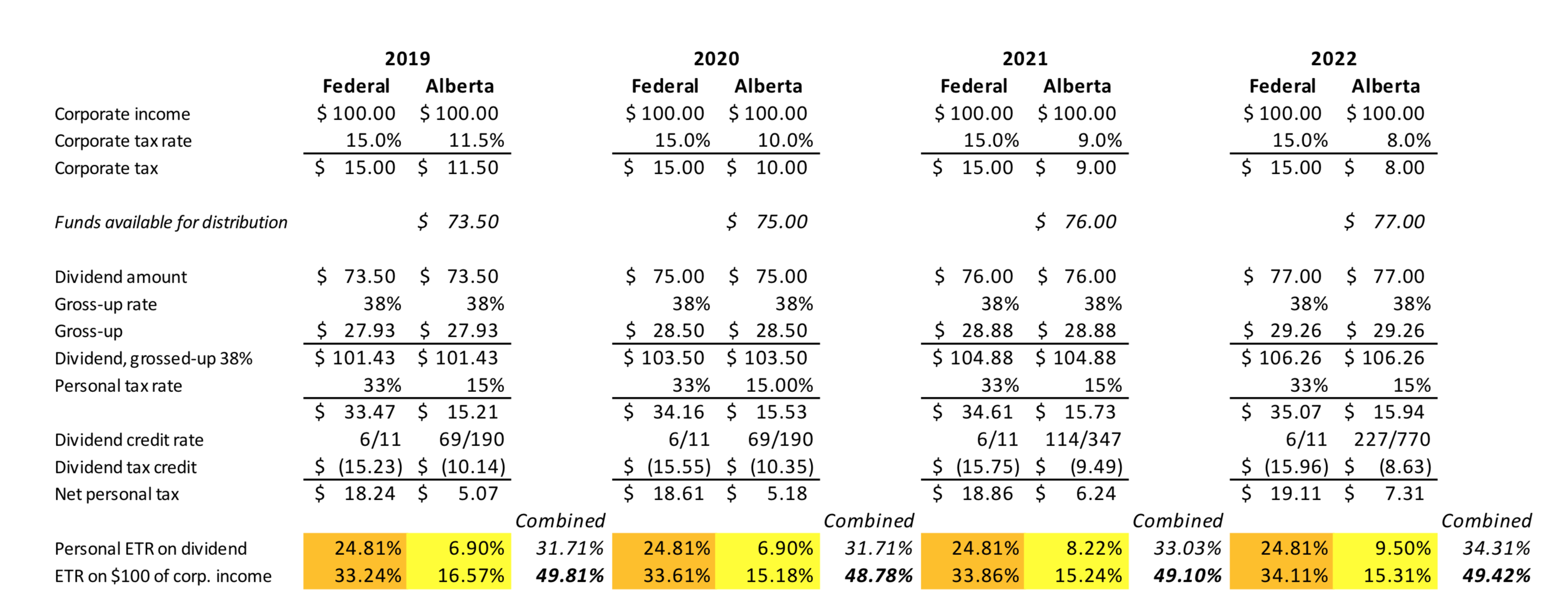

Probably recognizing that the previous Government had caused integration to be out-of-whack with its corporate tax rate increase to 12%, the current Government kept the dividend tax credit for eligible dividends unchanged at its pre-2015 level. Then, in the 2019 Alberta Budget, the Government announced that it would begin adjusting the eligible dividend tax credit in 2021 and 2022 after the Alberta general corporate tax rate drops below the pre-2015 rate of 10%. The new dividend tax credit rates were released with Bill 20 to be 114/347 and 227/770 of the gross-up for 2021 and 2022, respectively. This steadies the total integrated Alberta tax burden to approximately 15%, the same as the top Alberta personal tax rate, with the following result (assuming a calendar year-end for the subject corporation):

(click here to download table in PDF file)

While Alberta returns closer to integration in 2020 and subsequent years (total rate of 15%), the federal tax burden begins to depart from integration (i.e. going above the top federal tax rate of 33%) due to the imperfect mechanics of using a national gross-up percentage across all provinces. But what is really interesting is to examine the increase to the effective personal tax rate on eligible dividends (due to the reduced dividend tax credit) required to maintain Alberta integration post-2020:

|

2019 |

2020 |

2021 |

2022 |

|

|

Effective tax rate on eligible dividend after gross-up and dividend tax credit |

31.71% |

31.71% |

33.03% |

34.31% |

To achieve integration in an environment of declining general corporate tax rates, the eligible dividend tax credit must decrease, increasing personal tax on dividends. This creates a fairly significant reverse-arbitrage trap for unpaid corporate retained earnings as of January 1, 2021. In other words, pre-2021 corporate retained earnings that have been subject to the general corporate tax rate of 10% or higher, if paid out as dividend in 2021 or 2022, qualify for a reduced dividend tax credit that assumes the earnings had been subject to 9% or 8%. For example, $100 of 2020 retained earning would have been subject to $34.31 of tax rather than $31.71 if dividend distribution is delayed until 2022 or after – the extra $2.60 represents a whopping 8% increase in tax. To avoid this trap, large private corporations and public corporations should consider paying out as much of their retained earnings as taxable dividends before 2021. Of course, they must consider many other tax and non-tax factors before finalizing that decision.

Aside from this quirk, the reduction of the Alberta general corporate tax to 8% will make Alberta stand apart from its provincial peers with general corporate tax rates ranging from 11.5% to 16%. Hopefully, this “Alberta Advantage” will help Alberta attract much-needed investments and capital to re-boost its economy.

Related Blogs

Have you ever wondered how much your US citizenship is costing you? Why renouncing could save you hundreds of thousands and open new doors for financial opportunities.

As US expats prepare for another expensive and stressful tax filing season, we’ve compiled a list of...

Looking to make 2024 your last filing year for US taxes? Here’s what you need to do.

In a recent survey, one in five US expats (20%) is considering or planning to renounce their...

Travelling to the US? If you’re a US expat who doesn’t renounce properly, your trip may never get off the ground.

Air travel can be stressful. Rising airfares and hotel costs, flight cancellations, pilot strikes, long security wait...